Q3 2021 Market Update and Q4 Outlook - By Kurt S. Altrichter, CRPS®

- Kurt S. Altrichter, CRPS®

- Oct 6, 2021

- 8 min read

Updated: Jan 4, 2022

The S&P 500 hit new all-time highs again in the third quarter as investors looked past a resurgence of COVID-19 cases in the U.S. and instead focused on the positive combination of a resilient economic recovery, ongoing historic support from the Federal Reserve, and strong corporate earnings. Market volatility did notably pick up during the final few weeks of September, however, reminding investors that the transition to a post-pandemic “new normal” isn’t always going to be smooth.

Stocks moved steadily higher to start the third quarter as the U.S. economy continued to return to pre-pandemic levels of activity while corporate earnings remained solid. To that point, second quarter earnings results, which were released in mid-to-late July, were stronger than expected and broadly did not show signs of the margin compression that some analysts feared might hurt corporate profitability. Additionally, at the July FOMC meeting, Fed Chair Powell reiterated that, despite economic progress, it was not yet time for the Fed to begin to reduce Quantitative Easing (QE), thereby ensuring the economy and markets would continue to enjoy full Fed support until late 2021. Those factors helped investors look past an increase in COVID-19 cases, especially across the Sunbelt, as the S&P 500 hit a new all-time high in late July.

That positive momentum for markets continued in August, powered by similar factors: Positive corporate commentary, solid economic activity, and continued supportive Fed rhetoric. Those forces again combined to help markets look past a further increase in COVID-19 cases. Unlike during the COVID-19 waves of 2020 and early 2021, government authorities did not re-impose economic restrictions or lockdowns in response to rising case counts. Instead, most policy responses centered around mask mandates, and as such, the economic headwinds from rising COVID-19 cases were mild compared to previous episodes.

Meanwhile, politics once again became a focus of the markets in August. The Senate passed a $3.5 trillion budget reconciliation bill that would be the framework for potential changes to tax rates, entitlements, and climate policy. But what passed in August merely set the stage for the looming policy battle once Congress returned from the summer recess. Given that, stocks were able to look past future policy risks and climb steadily higher throughout the month with the S&P 500 ending August essentially at all-time highs.

The market tone changed in September, however, as many of the positive factors that supported stocks earlier in the quarter began to fade. First, corporate commentary turned more cautious last month. Profit warnings that cited supply chain constraints and margin compression came from multiple industries, and that caused investors to become more concerned about the outlook for corporate earnings. Then, economic data from August showed that the rise in COVID-19 cases had weighed slightly on the economic recovery. Finally, after investors ignored the looming policy battle in August, politics once again became an influence on markets as Democrats unveiled new details on a $3.5 trillion spending and tax plan that included increases to the corporate tax, personal income taxes for high earners, and changes to capital gains and inheritance taxes. Those factors weighed on markets initially in September, but the volatility was compounded by the news that the second-largest property developer in China, Evergrande, was likely going to default on debt payments. Fear of potential financial market contagion hit stocks in late September and the S&P 500 suffered its first 5% pullback in nearly a year. Markets remained volatile into the end of the quarter as the Federal Reserve confirmed market expectations that it will begin to reduce Quantitative Easing before year-end, while Washington approached the looming deadline of a government shutdown with no extension in sight, although that was avoided in the last few days of the quarter. The S&P 500 finished September with moderate losses although the index still logged a positive return for the third quarter.

In sum, the market remained resilient in the third quarter, but the final few weeks of September served as a reminder to investors that markets will face the resolution of numerous macroeconomic unknowns in the fourth quarter, and while fundamentals remain decidedly positive, an increase in market volatility should be expected.

Third Quarter Performance Review

The last few days of the third quarter had a substantial impact on quarterly index returns. For the majority of the third quarter, the Nasdaq had solidly outperformed both the S&P 500 and the Dow Jones Industrial Average as investors continued a trend from the second quarter by moving to less economically sensitive large-cap tech shares. However, during the last week of the quarter, as global bond yields rose, there was heavy selling in tech shares as investors rotated into other market sectors. The Nasdaq still slightly outperformed the S&P 500 while the Dow Jones Industrial Average produced a negative return for the third quarter thanks to the late September sell-off.

By market capitalization, large-cap stocks outperformed small-cap stocks in the third quarter. In fact, small-cap stocks had a negative return for the quarter as rising COVID-19 cases, mixed economic data, and the prospects of eventually higher interest rates caused investors to favor large-cap stocks as the outlook for future economic growth became less certain.

From an investment-style standpoint, growth outperformed value in the third quarter, thanks to tech sector gains, although the amount of that outperformance shrunk considerably during the final week of the quarter as tech shares declined.

On a sector level, performance was more mixed than the previous two quarters as six of the 11 S&P 500 sectors realized positive returns in the third quarter, with financials leading the way higher. For much of the third quarter, the tech sector outperformed, but as bond yields rose in late September, financial stocks rallied on the prospect of higher interest rates and overtook tech as the best performing sector in the quarter. Healthcare also performed well, bolstered by strength in pharmaceutical stocks following more COVID-19 vaccine mandates and booster shot approvals.

Sector laggards included the industrials and the materials sectors, both of which finished with negative returns for the third quarter. Uncertainty surrounding the strength of the ongoing economic recovery in the face of higher COVID cases pressured industrials initially in the third quarter, as did a lack of passage of the $1 trillion bipartisan infrastructure bill. Meanwhile, the materials sector declined late in the third quarter on Chinese economic growth concerns following the Evergrande debt drama. Broadly speaking, cyclical sectors, those most sensitive to changes in economic growth, lagged more defensive sectors in the third quarter due to the uncertainty of the economic recovery in the face of the COVID wave in July and August.

Internationally, foreign markets declined in the third quarter. Emerging markets dropped sharply, initially on concerns that rising COVID-19 cases would derail the global recovery, but late in the quarter, emerging markets fell even further on Chinese growth worries that stemmed from the Evergrande debt issues. Foreign developed markets, meanwhile, declined modestly during the final few weeks of the quarter on general global growth concerns combined with potentially higher global interest rates.

Commodities posted strong gains for the fourth quarter in a row and again outperformed the S&P 500 over the past three months. Major commodity indices were led higher by a late-quarter rally in oil prices as members of “OPEC+” maintained a historically high compliance rate to self-imposed production targets while easing COVID-19 cases around the globe in September bolstered the demand outlook for refined petroleum products. Additionally, there was no progress on nuclear negotiations between the U.S. and Iran, and sanctions remained in place preventing Iran from selling oil on the global market. Meanwhile, gold posted a small loss in the third quarter as a firming dollar and rising interest rates helped offset still stubbornly elevated inflation metrics.

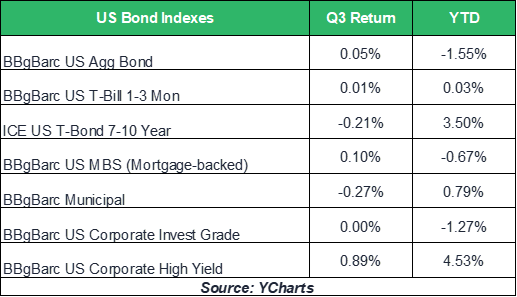

Switching to fixed income markets, most bond classes were little changed in the third quarter. The majority of bond indices were solidly higher through mid-September as investors rotated to safety following the rise in COVID-19 cases in July and August. But in late September, the Federal Reserve. confirmed tapering of Quantitative Easing will begin this year. That, combined with still-high inflation statistics, weighed on fixed income markets during the final few days of the third quarter which erased most of the quarter-to-date returns for many bond indices.

Looking deeper into the bond markets, longer-duration bonds and shorter duration bonds had very similar returns in the third quarter. For most of the quarter, longer-term bonds outperformed shorterterm bonds on the growing expectation that the Fed would begin to taper QE late in 2021, and that interest rates would start to rise in late 2022. But the late-September rise in global bond yields resulted in a moderate drop in longer-dated bonds, which erased the earlier outperformance over short-duration bonds.

In the corporate debt markets, higher-yielding, lower-quality bonds outperformed investment-grade bonds thanks to a late September drop in investment-grade following the rise in global bond yields, as investors rotated out of lower-yielding, yet higher-credit quality corporate debt as global yields rose.

Fourth Quarter Market Outlook

Market performance in the third quarter reflected continued improvement in the macroeconomic outlook as society, the economy, and risk assets showed resilience in the face of another wave of COVID-19, while corporate earnings were better than expected.

“However, that resilient performance should not be taken as a signal that risks no longer remain. In fact, the next three months will bring important clarity on several unknowns including future Federal Reserve policy, taxes, the pandemic, and inflation.”

The Federal Reserve has communicated that it will begin to taper Quantitative Easing in the fourth quarter, but markets do not yet know when exactly the Fed will start to scale back those asset purchases or the pace at which they will be reduced. If the Fed starts to taper QE sooner than expected, or the pace of reductions is faster than the market has currently priced in, it will cause additional volatility.

Meanwhile, in the third quarter investors were reminded that politics can be a powerful influence on markets, and over the next several weeks we will learn whether the debt ceiling is extended and if there will be any significant tax increases. If policies from Washington are viewed as negative for corporate earnings or consumer spending, they will cause a rise in market volatility.

Regarding the still ongoing pandemic, COVID-19 remains a risk for the economy and the markets. Positively, effective vaccines have allowed policymakers to avoid re-implementing economic lockdowns that could hurt corporate earnings and the economy. But the risk remains that a new COVID-19 variant renders the vaccines less effective and that would put the economic recovery in jeopardy.

Finally, inflation remains elevated and at multi-decade highs, and that combined with continued supply chain disruptions, due to the ongoing pandemic, is starting to impact corporate margins and profitability. If an increasing number of companies warn about future profitability due to these factors during the upcoming third-quarter earnings season, it will negatively impact markets.

Yet while risks remain, as they always do, macroeconomic fundamentals are still decidedly positive and it is important to remember that a well-executed and diversified, long-term financial plan can overcome bouts of even intense volatility such as we’ve seen over the last two years.

We understand the risks facing both the markets and the economy, and we are committed to helping you effectively navigate this still-challenging investment environment. Successful investing is a marathon, not a sprint, and even temporary bouts of volatility like we experienced during the height of the pandemic are unlikely to alter a diversified approach set up to meet your long-term investment goals.

Therefore, it’s critical for you to stay invested, remain patient, and stick to the plan, as we’ve worked with you to establish a unique, personal allocation target based on your financial position, risk tolerance, and investment timeline.

The economic and medical progress achieved so far in 2021 notwithstanding, we remain vigilant towards risks to portfolios and the economy, and we thank you for your ongoing confidence and trust. Rest assured that our entire team will remain dedicated to helping you successfully navigate this market environment.

Download a copy of this publication below.

Please do not hesitate to me with any questions or comments.

Schedule a portfolio review directly on my calendar (CLICK HERE)

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Direct: 952.828.5336

Email: kurt@ivoryhill.com

—Written 10.06.2021.

Comments