January Market Expectations

- Kurt S. Altrichter, CRPS®

- Jan 10, 2024

- 6 min read

The Ivory Hill RiskSIGNAL™ remains green since December 5th.

This week, our short- and mid-term signals have shifted back to green.

We are fully invested in this market and are favoring more risk and higher beta stocks as volatility remains suppressed (for now).

The VIX saw a significant start to the year, surging 17% last week from early-week lows before retreating below the crucial 14 level.

This rally in the VIX was supported by a rise in the RSI indicator, indicating the potential for a sustained uptrend in early 2024.

However, Friday's "outside reversal" on the daily chart, with the VIX hitting its highest point since mid-November before closing below Thursday's low, suggests possible exhaustion in the trend.

To confirm a VIX pullback and a more favorable trading environment for equities, a move below Friday's intraday low of 13.29 is needed. Additionally, watch for a new "unconfirmed high" in the VIX, which, if it occurs with the RSI remaining below its 2024 high of 58, could provide valuable guidance, as similar patterns preceded market movements in recent months.

Why Did Stocks Drop to Start 2024?

Markets started 2024 with the S&P 500 falling 1% while bubble-cap tech traded even worse, with the Nasdaq selling off more than 3% last week. Importantly, this decline wasn't triggered by any negative events but rather because the initial data points for 2024 didn't align with the aggressive and unrealistic expectations set for the year.

It's important to note that the S&P 500 had already surged by more than 11% in the fourth quarter of 2023, with the majority of that rally occurring between late October and December. Achieving an 11% gain in a year is substantial, let alone within just two months, so it's reasonable to experience sell off at the start of the new year, which indeed occurred.

Market Expectations

The first Market Expectations Table of 2024 (based on fundamentals) makes it clear that today's market is pretty straightforward. Investors have VERY high hopes, high confidence that interest rates will go down, the economy will grow well, and inflation will stay in check. If these assumptions are correct, we should see the S&P 500 challenge nominal all-time highs.

However, if these assumptions prove to be incorrect, investors should be prepared for a potential downward spiral, as the distance to reach fundamental support is quite substantial.

The Market Expectations Table shows that, unlike the past few years, there aren't many factors influencing stocks and bonds right now.

It boils down to three macro influences: what the Fed does with interest rates, how the economy is doing (Hard or Soft Landing), and whether inflation becomes a problem again or not.

What's notably absent from the equation are 1) Treasury yields, 2) Geopolitical issues, and 3) Domestic politics. These factors are grabbing headlines, but they aren't exerting a major impact on the markets for specific reasons.

First, Treasury yields are no longer surging independently; instead, they are primarily reflecting changes in economic growth, inflation expectations, and anticipated Federal Reserve actions.

Second, while geopolitical headlines are concerning, particularly concerning the potential for broader conflicts in the Middle East, the market doesn't seem to be reacting. Unless we see a significant spike in oil prices, geopolitics are unlikely to have a substantial influence on the markets, despite their media coverage.

Lastly, when it comes to domestic politics, it's expected to become a market influence later in the year. However, at present, the market doesn't perceive a high likelihood of a government shutdown or other funding-related dramas. This perception is driven by the fact that neither political party currently sees it as in their best interest to engage in such actions.

So, at the moment, the primary macro influences are Fed policy expectations, economic growth, and inflation.

The Q4 2023 surge in stock prices since October has been driven by very positive assumptions regarding these factors.

However, there's a potential issue here: the market has priced in these assumptions as if they are already a reality, which is not the case yet.

In essence, whether the markets maintain and absorb the gains from the last quarter or give them up – possibly give up a lot – will depend on how the actual facts unfold in the new year compared to these very optimistic expectations.

It's a crucial period where reality needs to align with these positive assumptions for the market rally to continue.

Current Situation:

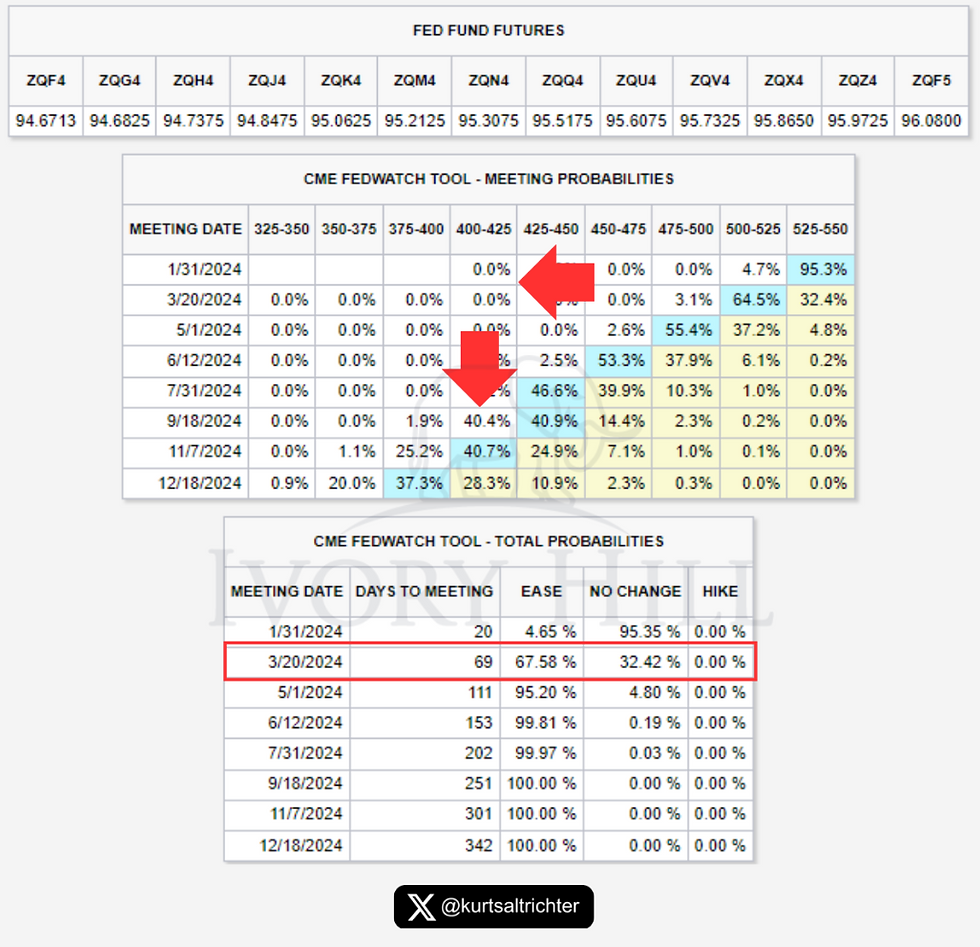

As of now, the Federal Reserve has taken a dovish stance, and the markets are operating under the assumption of a rate cut in March, with a total of four to six rate cuts expected in 2024. Economic growth is holding steady in what can be described as a "Goldilocks" scenario, remaining consistently positive. Additionally, inflation is on a downward trend, moving closer to the Federal Reserve's target of 2%, which opens the door for potential rate cuts.

The current situation aligns with the optimistic assumptions made by investors regarding rate cuts, economic growth, and inflation. If the actual facts unfold in a manner that supports these assumptions, it will contribute to solidifying the gains witnessed in the fourth quarter.

However, it's essential to note that this doesn't necessarily mean a continuous surge in stock prices but rather a reinforcement of the existing gains. This is still positive as it reduces the risk of significant pullbacks and lays the groundwork for a potential rally later in 2024.

Conditions Improve If:

Conditions improve if the Federal Reserve begins to signal a rate cut in March, economic data continues to exhibit a Goldilocks-like balance, and inflation keeps falling towards the Fed's 2% target. In such an environment, it would strongly validate the assumptions about the Federal Reserve's actions, economic growth, and inflation being correct. This could potentially push the S&P 500 towards a reasonable ceiling of around 4,900.

This situation would essentially represent an ideal backdrop for the stock market, characterized by a dovish Federal Reserve (implying a safety net for the market), robust economic growth, and declining inflation. Under these conditions, it wouldn't be unreasonable or unwarranted for the S&P 500 to reach new all-time highs, possibly surpassing 4,800 points.

Conditions Deteriorate If:

The situation could take a turn for the worse if several factors come into play. Firstly, if the Federal Reserve strongly opposes the idea of rate cuts in March (likely) and throughout 2024, it would go against the current market expectations. Secondly, if economic growth suddenly takes a downturn, it could disrupt the current equilibrium. Lastly, if inflation metrics, such as the CPI and Core PCE Price Index, rebound unexpectedly, it would contradict the assumption of declining inflation.

In this scenario, the very foundations of the Q4 rally would be undermined. This could lead to substantial declines in stock prices, and the possibility of giving back much of the gains seen from October to December would become a real concern. While it may seem unlikely given the strong investor confidence in the assumptions mentioned earlier, it's a scenario that should be taken seriously as it could become a reality if economic data takes an unexpected negative turn.

Small-Caps - Rejected Again

The soft landing narrative that had been driving the year-end rally in small-cap stocks has indeed lost momentum and failed to break out, in line with my earlier analysis.

This occurred simultaneously with sectors like utilities, staples, healthcare, and other defensive areas starting to show signs of breaking out.

These developments collectively convey a clear picture that higher volatility conditions could be coming to this market soon.

It's essential to recognize that a broadening bull market cannot solely rely on the leadership of overinflated tech giants. To ensure the market's broad health, it's imperative that the smaller, less capitalized indexes, establish and maintain a sustained upward trend.

Until small-caps have a sustained rally over a few months and quarters (not days or weeks), I do not consider this a bull market.

As evident from the chart provided below, there has been a noticeable deterioration in upside momentum, notably marked by the violation of the uptrend last week.

The small-cap Russell 2000 index experienced a significant pullback last week, breaking below the uptrend line that had been in place since the October lows.

Nonetheless, the 52-week highs reached in late December suggest that, over medium and longer timeframes, the prevailing direction of least resistance remains upward.

Even if small-cap stocks don't experience an immediate broadening, the overall market outlook remains positive for the intermediate-term. Presently, any pullback on the S&P 500 towards the 4,500-4,600 range should be seen as an opportunity for increased equity exposure.

This perspective is grounded in several factors supporting the positive outlook for stocks: 1) Strong economic growth, 2) A more dovish stance from the Federal Reserve, and 3) Inflation continuing to fall.

However, the challenge for the market in early 2024 lies in the fact that this optimistic outlook does not justify a 19.5X multiple valuation.

To be clear: the market's short-term issue is that it has priced in expectations of rate cuts in March (unlikely) and a scenario of Immaculate Disinflation (a situation where the Fed successfully brings down inflation without causing a recession or high levels of unemployment), characterized by falling inflation and stable growth. If the incoming data doesn't align with these expectations, as was the case last week, stock prices will fall.

It’s essential to recognize that just because the outlook isn't flawless, it doesn't mean it's not still favorable.

However, at the moment, given the lofty market expectations and my concerns regarding a possible growth slowdown, if our short- and mid-term volatility signals turn red, our objective would be to increase exposure to quality (SPHQ/QUAL), lower-volatility (SPLV), value (VTV) and sectors such as Utilities (XLU), Consumer Staples (XLP), Real Estate (XLRE), equally-weighted S&P 500 ETF (RSP) over the market cap weighted SPY. This strategic approach aims to mitigate volatility and minimize downside risk in the portfolio without moving out of equities.

And remember - The one fact pertaining to all conditions is that they will change.

Feel free to use me as a sounding board.

Best regards,

-Kurt

Kurt S. Altrichter, CRPS®

Fiduciary Advisor | President

Comments